Dividends are a way for companies to return a portion of their profits to shareholders. Call it a cash reward for being an investor—each allotment is often paid out as small amounts per share.

I like to explain the concept by sharing a story about my 8-year-old son. One day, he noticed a dollar coin on the ground. Lying next to it was a lonely old beat-up penny. He bent down but only picked up the dollar. “What about the penny?” I asked. “Dad, a penny doesn’t even buy a piece of candy these days,” he scoffed.

My son’s catch-and-release treasure hunt was a wake-up call for me—the youth have no love for the coin of the realm. Instead, it’s all about the Benjamins. Or, at least, the Washingtons. Dividends, however, make the counterargument: cents make sense.

How Dividends Work

It’s not uncommon for a company to pay a dividend of, let’s say, 50 or 60 cents per share, divided into four quarterly payments. Like my own children, the general public sometimes fails to appreciate a decimal point distribution. After all, does the dusty coin jar really affect your bottom line?

Perhaps even more underappreciated is the dividend increase, typically only bumping up a few cents in any given year. If a company announces a dividend boost from 57 to 61 cents, stockholders get an extra four cents per share. Four extra cents may seem insignificant, but it equates to a 7% dividend gain on each share. If the amount increased by 7% yearly, it would only take about a decade to double. In other words, if you stick with dividends, dividends typically stick with you.

The Study: Dividend Income Vs. Bond Interest

Bonds are essentially IOUs issued by governments or companies. Investors buy them, and the issuer promises to repay in full, plus interest. The pro is that the risk and volatility are often lower than in equities, but the con is that the reward often is, too.

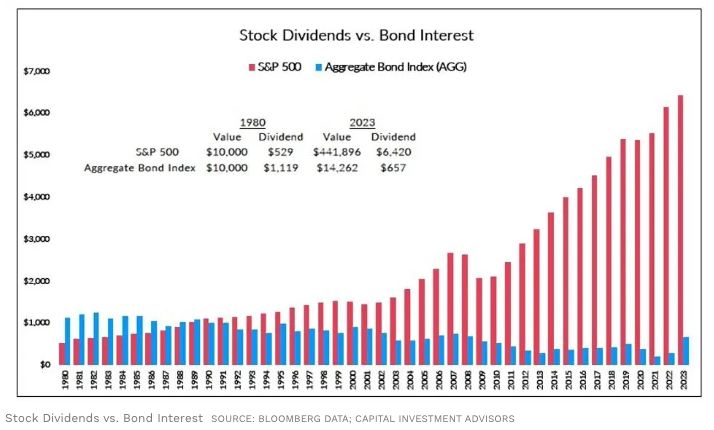

How does bond interest stack up against the income-producing potential of stock dividends? Examining a $10,000 investment in the S&P 500 vs. the Aggregate Bond Index, my team at Capital Investment Advisors charted the results over more than 40 years. In each case, investors left the principal alone while taking the annual cash income.

The table below illustrates each investment’s progress over time.

Comparing Investments

In 1980, a $10,000 investment in the S&P 500 paid a yearly dividend of about $529—5.29% of the initial investment. Forty-four years later, it had climbed to $6,420—a 64% annual yield on the original investment. And that the original investment itself grew as well. A $10,000 holding in the S&P 500 in 1980 would have blossomed to nearly $441,900, plus the annual dividend income.

On the other hand, the Aggregate Bond Index only grew from $10,000 to $14,262 and would now pay out just $657 per year, or 6.57% on the original investment. Stock dividend income clearly outpaced bond interest. Annual stock dividend payouts increased more than 12 times, while the remaining price-only return grew 44 times. On the other hand, bonds rose less than 1.5 times in price, with an income reduction of about 41%.

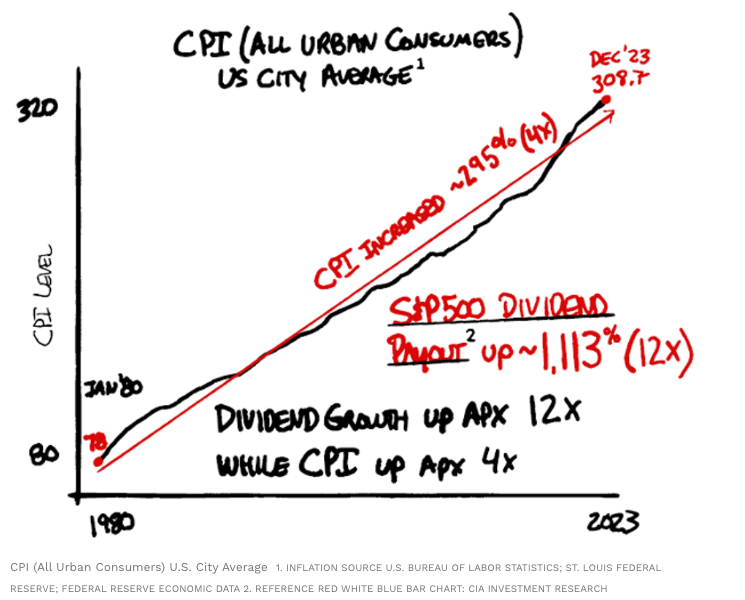

Inflation increased by about four times between 1980 and 2023, but the S&P 500 dividend payout rose by 12 times. Accelerating three times faster than inflation, dividend stocks protected the purchasing power of investors. Whether your retirement portfolio holds $500,000 or $5 million, it’s hard to find a more consistent way to outpace inflation than rising stock dividends.

The Verdict: Dividends Can Be A Powerful Wealth-Building Source

Those surprised by the above statistics are better served using them as a guide for future decisions rather than a source of regret for lost earnings. The typical 40- or 50-year-old still has ample time to earn money in the market. And regardless of age, you may have more years of spending ahead than you think.

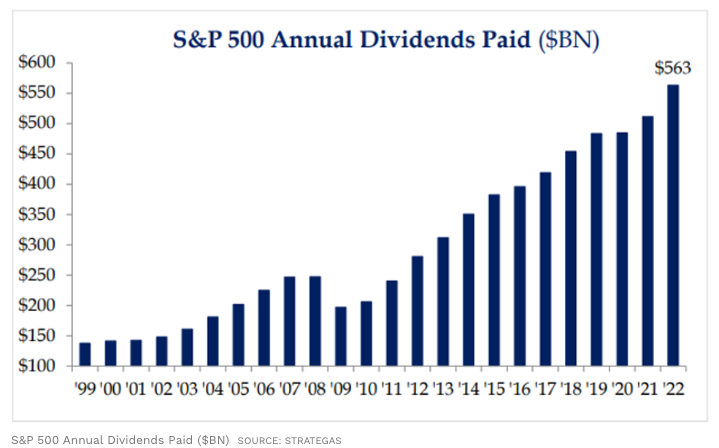

Look for stocks that are perennial dividend payers and consistent dividend growers. Then, be patient and watch the dividends roll in over time. Remember, despite price fluctuation, dividends from established American companies tend to remain relatively steady, even in tumultuous years like 2020 and 2022. The following chart shows the persistent rise of aggregate dividends paid from the S&P 500 from 1999 through 2022. Although there have not been aggregate dividend raises every single year, the trend over time is clear.

Aggregate Annual S&P 500 Dividends Paid

The Bottom Line

Act calmly, deliberately, and with purpose. You’ll find that those pennies add up over the years, and you’ll likely be happy you picked them up. Pursuing dividends can be rewarding for any investor with enough long-term vision to let the spare coins become treasure.

This information is provided to you as a resource for informational purposes only and is not to be viewed as investment advice or recommendations. Investing involves risk, including the possible loss of principal. There is no guarantee offered that investment return, yield, or performance will be achieved. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. For stocks paying dividends, dividends are not guaranteed, and can increase, decrease, or be eliminated without notice. Fixed-income securities involve interest rate, credit, inflation, and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed-income securities falls. Past performance is not indicative of future results when considering any investment vehicle. This information is being presented without consideration of the investment objectives, risk tolerance, or financial circumstances of any specific investor and might not be suitable for all investors. There are many aspects and criteria that must be examined and considered before investing. Investment decisions should not be made solely based on information contained in this article. This information is not intended to, and should not, form a primary basis for any investment decision that you may make. Always consult your own legal, tax, or investment advisor before making any investment/tax/estate/financial planning considerations or decisions. The information contained in the article is strictly an opinion and it is not known whether the strategies will be successful. The views and opinions expressed are for educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions.